European ceramics pay the price of unsustainable sustainability

The European Commission’s new ETS benchmarks undermine the competitiveness and international market presence of the European ceramic industry, putting the sector’s very survival at risk.

by Paola Giacomini

• The new ETS benchmarks: a methodological impasse

• The economic impact on the Italian and Spanish ceramic industry

• European production at risk

• How much does the European ceramic industry pollute?

• Carbon leakage: the European paradox

• The Manifesto “For the future of European ceramics”

As the process leading to the revision of the EU Emissions Trading System (ETS) for the 2026–2030 period approaches a critical phase, the draft reform proposals circulated by the European Commission at the end of March came as a cold shower for Italian and Spanish ceramic tile manufacturers attending Coverings in Las Vegas.

Just one week earlier, on 25 March in Brussels, delegations representing the two major industrial systems of European ceramics—led by ASCER and Confindustria Ceramica, together with their respective territorial institutions, the Emilia-Romagna Region and the Generalitat Valenciana—had gained broad, cross-party support from the main groups of the European Parliament for the proposals set out in the manifesto “For the Future of European Ceramics”, jointly signed by the two Regions.

While fully acknowledging the legitimacy and necessity of the European Union’s environmental objectives, the document highlights the very real risks to the industrial sustainability of the European ceramic industry if the new regulatory framework continues to follow an approach that fails to take into account the technological and market-specific characteristics of the ceramic sector.

For now, all of these proposals and requests have been rejected and sent back to the proponents—a decision that Italian and Spanish manufacturers describe as being completely “detached from industrial reality” and destined to produce highly punitive effects on a sector already under enormous cost pressure, particularly with regard to energy.

Press briefing with the top management of Confindustria Ceramica at Coverings 2026.

The new ETS benchmarks: a methodological impasse

The most critical aspect of the regulatory update concerns the revision of the benchmarks used to allocate free CO₂ allowances to companies exposed to the risk of carbon leakage, such as the ceramic industry. What is being challenged is the implicit assumption underlying the ETS reform—namely, that technologies enabling a further drastic reduction in emissions are already available, when in fact they are not.

The new benchmarks are clearly unrealistic, as they refer to the energy performance of plants operating in other industrial sectors, achievable only through technologies that are not applicable to ceramic production—for example, the widespread use of biomass as an energy source.

“This is a deeply flawed approach,” said Alberto Echavarria, Secretary General of ASCER, the Spanish ceramic tile manufacturers’ association, “because the ceramic sector, due to technological constraints and objective limits in resource availability, is not able to use biomass as an alternative fuel.”

Applying these benchmarks would therefore result in a further significant reduction in free allowances, leading to higher ETS-related costs for emissions that, at present, cannot be further reduced due to the lack of alternative technological solutions deployable on a large scale (such as renewable hydrogen, electrification of thermal processes, or access to decarbonised energy carriers).

This point had also been stressed by Renaud Batier, Director General of Cerame-Unie (the European Ceramic Industry Association), in his address to the European Parliament on 25 March. He highlighted that

“the electrification of ceramic kilns is not yet a mature technology for ceramic production, not to mention the insufficient capacity of the electricity grid or the fact that electricity costs three times as much as natural gas. The tools for the transition are simply not ready yet from a technological and economic standpoint,” he concluded.

A further paradox lies in the fact that the ceramic sector is recognised by EU legislation as “hard to abate” precisely because, to date, there are no alternative technologies capable of delivering further significant emission reductions beyond the energy efficiency measures already widely implemented.

“This is a mechanism that penalises the most efficient and virtuous ceramic companies. We would be forced to pay an extremely high price for a transition that we are technically unable to achieve within the proposed timelines,”

said Graziano Verdi, Vice President of Confindustria Ceramica and President of CET, the European Ceramic Tile Manufacturers’ Association.

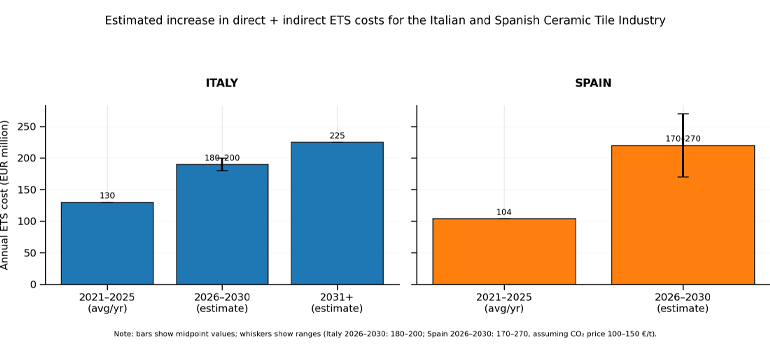

The economic impact on the Italian and Spanish ceramic industry

Designed to incentivise decarbonisation, the ETS system is in practice turning into a “production tax”, with carbon prices set by a highly financialised market, rising from €5–15/tCO₂ in 2018 to €74–77/t in April 2026 (with a peak of over €100/t in 2023 and €92/t in January this year), without a parallel strengthening of the industrial instruments needed to support the transition.

In this context, the reduction in free allowances resulting from the application of the new ETS benchmarks (estimated at around 32% less compared to the 2021–2025 period) will cause ETS costs to soar to levels that are virtually unsustainable in both Italy and Spain.

For the Italian ceramic tile industry, average annual ETS costs would rise from around €130 million in the 2021–2025 period to €180–200 million in the 2026–2030 five-year period, and then climb to approximately €225 million from 2031 onwards.

In other words, as highlighted by Confindustria Ceramica President Augusto Ciarrocchi, this would amount to

“around half of the annual investments of a sector that over the past decade has invested on average €400 million per year—about €4 billion in total, equal to 6.9% of average annual turnover.”

According to Italian manufacturers interviewed at Coverings, the impact of ETS costs on the production cost of one square metre of tiles could rise to around €1/m²—an increase that, in a highly competitive global market such as ceramics, is virtually impossible to pass on to customers.

An equally bleak picture emerges for companies in the Spanish ceramic cluster of Castellón. Here, according to estimates prepared by ASCER, direct and indirect ETS costs for an annual production of around 400 million square metres could rise from around €104 million/year in the 2021–2025 period to €170 million should the price per tonne of CO₂ reach €100 (and to even €270 million if the price of CO₂ climbs to €150).

And still within the Spanish ceramic district, these figures must be added to the costs that will be borne by producers of glazes, frits and colours, estimated by the trade association ANFFECC at around €55 million.

European production at risk

An economic impact of this magnitude will have serious repercussions that go well beyond the immediate erosion of ceramic companies’ profits.

At an industrial level, it first and foremost means undermining investments in product and process innovation (including those related to sustainability). In turn, this would translate into a loss of competitiveness and a gradual withdrawal from international markets, which are already highly competitive and contested by non-EU operators that often rely on environmental and social dumping practices.

“In a scenario like this,” - manufacturers argued at the Las Vegas trade fair - “it is impossible to believe that we can remain competitive in the North American market. Without a change of course, the risk is that many companies will no longer be able to sustain exports from European plants.”

In other words: there is a concrete risk of reduced European production and relocation, with obvious consequences for employment (and social) stability in ceramic districts.

“The situation is very serious,” said Alberto Selmi, Vice President of Confindustria Ceramica, “and never more than today are we aligned with trade unions and with our employees, for whom the risk of job losses is truly high.”

Clearly, the decline in investments (current and, above all, future) and in production will affect the entire upstream supply chain of the ceramic industry—manufacturers of plants, equipment and machinery, as well as suppliers of glazes and raw materials—which represent the other fundamental pillars of the ceramic districts of Sassuolo and Castellón.

One figure puts this into perspective: in 2024, against an estimated ETS cost of €120 million, the Italian ceramic tile industry reduced technological investments by more than €80 million.

“Europe risks losing a strategic industrial asset. We cannot afford to lose further industrial know-how: every skill that leaves Europe is a piece of competitiveness that will never come back,” said Paolo Lamberti, President of ACIMAC.

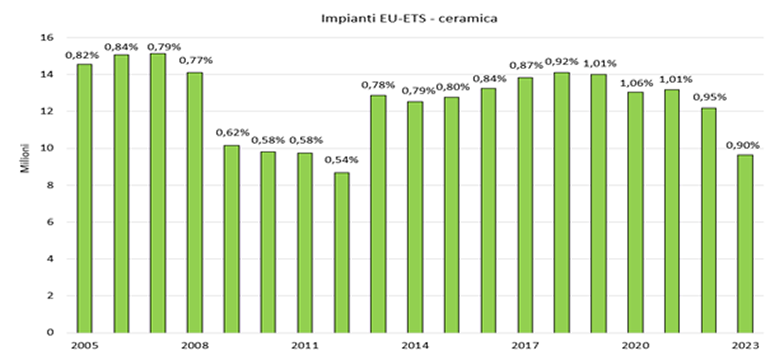

How much does the European ceramic industry pollute?

Very little, as shown by studies carried out by Nomisma Energia (fig. 1). It is a well-established fact that Italian and Spanish ceramic companies are those that have invested the most worldwide in reducing CO₂ emissions, achieving excellence also in terms of sustainability. Overall, European ceramic installations covered by the ETS system account for only 0.9% of total emissions, despite representing around 8% of the number of stationary installations regulated by the scheme. They are therefore small emitters, with average values per site among the lowest of all regulated industrial sectors (16,180 tCO₂/year). By way of comparison, the stationary installation with the highest emissions recorded in the ETS system emitted around 8,500,000 tCO₂ in 2024—an amount comparable to the total emissions of the entire European ceramic sector.

Regardless of the improvements already achieved in recent years in terms of energy efficiency, the ceramic industry nevertheless remains among the sectors most exposed to the distortive effects of the ETS mechanism. The challenge is not whether or how much to decarbonize—an objective that the European ceramic industry has amply demonstrated it shares—but how to do so without dismantling Europe’s industrial base.

source: Nomisma Energia

Carbon leakage: the European paradox

As currently conceived, the revision of the ETS system could cause more economic damage than environmental benefit, paradoxically producing the opposite effect to the one it was originally designed to achieve: reducing emissions. Or rather, it may reduce them in Europe if producing here becomes increasingly unsustainable—but it will increase them globally as a result of production relocation and rising imports of ceramic products from non EU countries that are subject to environmental and social constraints often far lower than those applied in Europe.

“Europe is scoring an own goal: we will end up importing polluting ceramics while giving up those produced in Europe under the highest sustainability standards,” says CET President Graziano Verdi.

The risk is very real, not least because there is no shortage of extra European competitors ready to supply a growing share of EU ceramic tile consumption, in some cases with significant excess production capacity. Just look at consumption data for 2024. In that year, European production covered 87% of tile demand across the 27 EU Member States (729 million square metres out of total consumption of 839 million). The remaining 110 million square metres were imported mainly from India (54 million) and Türkiye (39 million), with smaller volumes from Ukraine, Serbia, China, Egypt, Tunisia, the United Arab Emirates and Saudi Arabia.

It should also be noted that the European ceramic industry is not covered by CBAM (the Carbon Border Adjustment Mechanism), the tool through which the EU applies a carbon cost—equivalent to that borne by European producers under the ETS—to certain imported products (but not ceramics). This is one of the key points included in the manifesto “For the Future of European Ceramics” presented to the European Parliament. The request is for an application of CBAM to the ceramic sector that is properly integrated: a competitive rebalancing instrument capable of operating both on the internal market (between European companies subject to the ETS and non EU producers) and on global markets (through a mechanism compensating CO₂ costs on exports), at least until greater harmonisation of ETS systems is achieved at global level.

The Manifesto “For the future of European ceramics”:

The demands of the Italian and Spanish ceramic industry

- Freezing of current free allowance allocations.

- Suspension of the benchmark revision for the 2026–2030 period in order to redefine the criteria and introduction of a sector-specific fuel benchmark for the ceramic industry.

- For small emitters, raising the threshold for access to national equivalent measures (opt-out) from 25,000 to 50,000 tCO₂/year.

- Application of CBAM to the ceramic sector to safeguard the competitiveness of European companies both on the internal market and on non-EU markets.

- Creation of dedicated European funds for strategic research projects aimed at the decarbonisation of the ceramic sector.

Did you find this article useful?

Join the CWW community to receive the most important news from the global ceramic industry every two weeks

Related articles

Recent articles

Ceramic World Review 167/2026

Powtech Technopharm 2026

Main topics

Read more